Service financial management: ITIL 4 Practice Guide

Practice

Practice

- Practice

- ITIL

May 1, 2020 |

41 min read

- Practice

- ITIL

This document provides practical guidance for the service financial management practice.

1. About this document

It is split into five main sections, covering:

- general information about the practice

- the practice’s processes and activities and their roles in the service value chain

- the organizations and people involved in the practice

- the information and technology supporting the practice

- considerations for partners and suppliers for the practice.

1.1 ITIL® 4 qualification scheme

Selected content from this document is examinable as a part of the following syllabus:

- ITIL Leader – Digital and IT Strategy

Please refer to the syllabus document for details.

2. General information

2.1 Purpose and description

Key message |

The purpose of the service financial management practice is to support the organization’s strategies and plans for service management by ensuring that the organization’s financial resources and investments are being used effectively. |

The service financial management practice supports decision-making at many levels of the organization by providing reliable financial information. It provides visibility into the budgeting, costing, and accounting activities related to the products and services.

The practice is mainly concerned with the economics of services, including:

- understanding and optimizing the financial aspects of service delivery and consumption

- understanding and optimizing the costs of the organization’s products throughout their lifecycle

- providing high-quality financial information about products and services to stakeholders.

The practice typically does not cover those financial activities of an organization which are not directly related to the management of products and services, such as:

- investments and investment analysis

- credit, loans, and interest

- financial instruments that are not directly involved in product and service management.

The practice supports these financial management activities with information about products and services, associated costs and revenue, cost allocation and dynamics, and other relevant data, analysis, and forecasts.

The practice helps to ensure that the organization’s products and services are sufficiently funded by:

- providing information about the costs of products and services throughout their lifecycle

- planning and managing budgets for products and services

- anticipating and monitoring revenues from service delivery, if applicable.

The practice does not, however, include making funding decisions, prioritizing investments, or distributing profits. These decisions involve other practices, including the strategy management, risk management, and portfolio management practice.

Financial management in organizations is usually supported by specialized roles and organizational structures, such as finance, accounting, and financial analysis teams and structures. However, these teams are often focused on tax accounting, financial accounting, and compliance rather than on supporting the effective management of digital products and services. Teams that are involved in digital product and service management are likely to lack expertise in financial and commercial matters. This inconsistency in management focus and expertise is closely connected to the role of digital and IT in the organization.

Examples: |

|

The two example scenarios are extremes, and most organizations are somewhere in between. Either way, it is important to combine expertise in two areas:

- product and service management, with a particular focus on the following practices:

- architecture management

- workforce and talent management

- service configuration management

- IT asset management

- service level management

- suppler management

- financial management, with a particular focus on:

- management accounting

- budgeting

- financial analysis.

Organizational solutions for this include:

- including financial professionals (finance business partners) in digital product teams, focusing on the service financial management practice

- including digital and IT business partner(s) within the finance team, focusing on digital products and services

- including a dedicated finance team within the IT department, focusing on the service financial management practice and collaborating with the finance team in the wider organization

- providing special training and education in the service financial management practice for product and service managers and IT leaders.

2.2 Terms and concepts

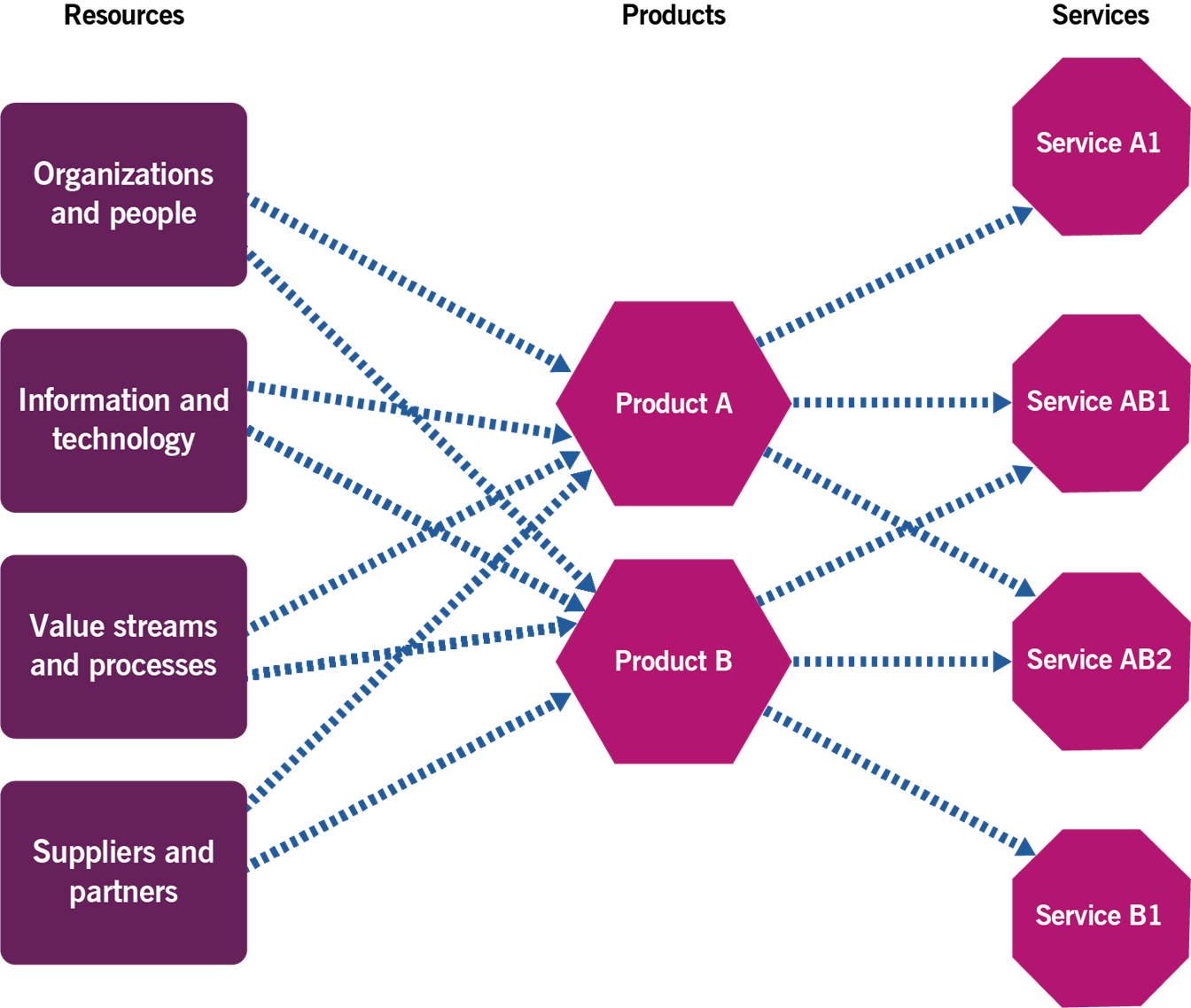

The service financial management practice helps decision-makers to understand and optimize the costs of digital products and services. This requires them to understand, capture, and model the:

- costs of resources used to create and deliver products and services

- distribution of the resources (and their costs) between products and services.

The resulting cost model is an important part of the organization’s approach to service financial management. An example is shown in Figure 2.1.

Figure 2.1 The costs of resources, products, and services

Once costs of products and services are understood, it is possible to allocate these costs to service consumers, customers and other cost objects.

Based on this financial information, organizations can:

- optimize planning, procurement and utilization of resources

- improve portfolio decisions

- plan, optimize and control budgets

- optimize charging

- align digital and IT resources, products and services to organizational strategy.

2.2.1 The cost of resources

ITIL 4 suggests organizing organizations’ resources into four groups, known as ‘the four dimensions of service management’. They are:

- organizations and people

- information and technology

- partners and suppliers

- value streams and processes.

All of the costs of all resources can be associated with one of these groups. From the management accounting and budgeting perspective, the four dimensions may be used as the highest-level categories to assign costs (known as ‘cost types’).

Definitions: |

Cost The amount of money spent on a specific activity or resource. Cost type The highest level of category to which costs are assigned in budgeting and accounting. |

Examples of cost elements in each of these categories include:

- organizations and people

- payroll

- travel

- training

- recruiting

- information and technology

- hardware

- software

- networks

- partners and suppliers

- external services

- value streams and processes

- management tools

- management activities.

The cost elements above should be documented with more detail, down to the specific costs. This will lead to the discovery of costs that belong to different cost types. When organizations define and agree their approach to the practice, they should provide guidance for these situations. For example:

- Training for organization’s employees may be provided by an external provider, which could be categorized as either a ‘people’ or ‘supplier’ cost type.

- An IT server could be provided in a cloud by an external provider, which could be categorized as either a ‘technology’ or ‘supplier’ cost type.

- An audit of a product may be conducted by a joint team that includes external and internal auditors, which could be categorized as a ‘management’, ‘people’, or ‘supplier’ cost type.

The rules for cost categorization should be included in the agreed service financial management approach. They should ensure that all relevant costs are accounted for in a logical and meaningful way, without omissions or duplications.

2.2.2 Direct and indirect costs

In Figure 2.1, the costs of resources are allocated to multiple products, and the costs of those products are allocated to multiple services. To understand the costs of products and services and make good management decisions, understanding the rules of the cost allocation is crucial. The basic classification of costs from the allocation perspective identifies two categories of costs: direct and indirect costs. Some of the indirect costs are overheads.

Definitions: |

Cost object |

| An item to which costs are allocated. Examples include products, services, service offerings, projects, customers, distribution channels, and so on. |

| Direct cost |

| A cost that is fully allocated to a cost object. |

| Indirect cost |

| The cost of a resource used by and therefore allocated to multiple cost objects. |

| Overhead |

Indirect costs which cannot be reasonably allocated to selected cost objects. |

Direct costs are fully allocated to a selected cost object. For example, 100% of the labour costs of teams working solely on one product are allocated to this product.

A significant part of the costs associated with digital and IT products and services is categorized as indirect; even more if service consumers are selected as cost objects. This makes the understanding and correct allocation of indirect cost a key enabler of the service financial management practice.

Some indirect costs can be reasonably allocated to selected cost objects using a fair and transparent driver. For example, the labour cost of a user support team can be reasonably allocated to individual services if all of the user support records have a correctly assigned ‘service’ attribute and timestamps. In this case, 100% of the support team’s work time could be distributed across the services which the team supports.

| Key message |

Cost drivers selected for the allocation of indirect costs should meet the following criteria:

|

In other cases, there is no reasonable way to allocate costs to selected cost objects. This is usually when doing so would use more resources than can be justified by the benefits this allocation might provide. For example, the costs of shared office spaces could be allocated to the services delivered by the organization by calculating how the space is used by various teams and how those teams contribute to products and services, but this calculation is unlikely to improve management information that is enough to be justifiable. These difficult-to-allocate indirect costs are known as overheads. Typically, examples include management costs, shared accommodation, and other shared services (such as catering, cleaning, security, and so on).

To understand the full costs of a cost object, after calculating the direct and indirect costs that can be reasonably allocated, a total overhead is usually distributed across the cost objects as agreed in the organization’s approach to the practice. It may be a simple even distribution or a function of the allocated costs, revenue, profit, or some other factor.

Key message |

In management accounting, decisions about cost allocation are made by the organization in a way that meets the decision-makers’ requirements. These include: • identifying cost objects • calculating the full cost of a cost object • allocating drivers for indirect costs • categorizing certain costs as overhead • allocating overhead to the cost objects. |

2.2.2.1 Activity-based costing

In many cases, reasonably allocating indirect costs is difficult because a significant part of the indirect costs are associated with people’s activities. Many teams in an organization contribute to the management of multiple products and services. Even if a team dedicates 100% of its resources to a single product (and those costs were categorized as ‘direct’ costs for that product), the same costs may also be categorized as ‘indirect’ for another cost object is chosen, such as the total cost of service provision to a customer. When this is the case and ‘people’ costs constitute a significant part of the overheads, the activity-based costing (ABC) method can be used to allocate the costs.

This method involves analysing all of the activities required to manage a product or deliver a service. The resources required to perform each activity (including both time and materials) are documented, the amount of each activity performed for each cost object is measured, and the agreed costs of that activity are allocated to the cost object.

This is an accurate, but expensive and complex, method. It should only be used if:

- the costs of people’s activities constitute a significant part of the overhead

- a better understanding of the cost distribution across the cost objects may result in a significant improvement in decision-making

- there are sufficiently reliable and affordable ways to calculate or estimate the allocation of people’s time to the selected cost objects.

2.2.3 Capital and operational costs

Capital costs or capital expenditure (Capex) is the cost of purchasing or creating resources that are recognized as financial assets, for example, computer equipment and buildings. The cost of fixed assets depreciates over multiple accounting periods, which is reflected in the cost of resources, products, and services in each period. Only depreciation (the agreed portion of the initial cost) is included in the costs in each period.

Operational costs or operational expenditure (Opex) is the cost that the organization incurs through its normal business operations. These costs typically include repeating payments, such as payroll and payments for supplier’s services. Operational costs of the period are fully included in the calculated costs of the respective resources, products, and services in the period.

In tax and financial accounting, the decision about whether to classify costs as capital or operational is not arbitrary. It is determined by enterprise financial policies that are based on generally accepted accounting practices, tax legislation, and the organization’s funding policies. Tax legislation provides rules about the minimum cost that qualifies as a capital cost, the number of years over which the investment can be spread, and by how much the cost may be depreciated each year. Accountants in the organization are qualified to understand these laws, policies, and funding decisions and to provide advice and guidance about how to apply them.

In management accounting, however, it may be appropriate to adjust the Capex accounting rules, or even apply the Capex rules for resources that are treated as Opex by the tax and financial accounting professionals, if this better reflects the actual lifecycle of the resources. For example, if the actual lifecycle of a resource is longer or shorter than the one defined by the legislation and spreading its cost across the adjusted number of periods would provide a more accurate understanding of the costs of the affected products and services.

2.2.4 Fixed and variable costs

Costs can be classified as fixed or variable. If selected cost objects are products and services, their fixed costs do not change when the service usage varies within a defined variation range. However, variable costs reflect variations in service consumption.

Costs can be classified as fixed or variable only in the context of a defined variation range. The range is usually limited by the capacity of the respective resources. For example, the cost of a software used by the organization does not change if the number of users increases, so long as it remains within the available license pool, so it is classified as a fixed cost. When the number of users reaches the limit of the license pool, a need to buy more resources (licenses) arises, so the cost should be classified as variable. Costs like these are known as ‘semi-variable’; most fixed costs are actually semi-variable and they change if service consumption exceeds a certain threshold.

Key message |

In management accounting, decisions about fixed and variable costs should reflect the capacity and elasticity of the organization’s resources, as well as the active terms and conditions of contracts with suppliers and partners. The organization’s approach to the service financial management practice should include practical guidance on the fixed/variable classification. |

Understanding cost variability is important for capacity planning and budgeting for products and services. For example, if business plans include growth in service consumption, budgets should include the respective expected growth of the relevant variable costs.

Organizations can manage a proportion of variable costs by making effective procurement decisions, such as choosing between buying resources or services and selecting cost-effective plans and tariffs.

In general, decreasing variable costs when demand for services is high is recommended. A good example is the choice between an ‘unlimited calls and data’ plan for a fixed price and a ‘pay-as-you-go’ plan; the former is better for a high level of service usage, the latter is more efficient if the service usage is low and occasional.

2.2.5 Budgeting and charging

Budgeting is an important part of an organization’s financial planning. It is the activity of estimating, target setting, and controlling the spending and earning of money during a particular period or initiative.

Budgeting consists of a periodic negotiation of future budgets and the ongoing monitoring and adjusting of current budgets.

Definition: Budget |

A documented estimate of all of the spending and earning of money during a particular period or initiative. |

Budgeting is the key mechanism of planning and providing funding for the resources necessary to meet the organization’s objectives. Budgeting answers fundamental business questions and helps to ensure that the answers are properly executed. Example questions include:

- Does the organization have the resources needed to meet its objectives?

- How many/much of the resources will we need and when?

- Where will the resources come from?

- For every period or milestone, what progress should the organization have made towards meeting its objectives?

- How should the organization adjust costs to reflect changes in service consumption?

Many of these questions cannot be answered without a good understanding of the organization’s costs. Good budgeting is based on a good cost model. However, budgeting is not limited to cost planning; it also includes estimating funding, whether it comes from sponsors (for example, an organization may sponsor all costs of its internal IT service delivery), service consumers paying for the services, or other sources.

If funding includes or is fully based on the revenue from service delivery, charging becomes an important subject of financial planning. It includes:

- Pricing: defining prices and the associated terms and conditions for the service offerings. This include defining price units (chargeable units of service consumption), tariffs and plans, payment options, and so on. Pricing options include:

- Cost-based pricing Prices for service consumers are defined based on estimated or actual costs of the services for the service provider

- Market prices are based on the established price level on a particular market

- Going rates reflect previous agreements between the service provider(s) and service consumer(s) and may be different from market prices

- Billing/invoicing: producing and issuing documents to service consumers informing them about the money they owe for the services provided, according to the agreed pricing and terms of payment.

If the agreed charging approach includes receiving money for the services provided from the service consumers, charging may also include activities such as collection and debt management. They are usually not included in the scope of the service financial management practice. However, information about payment-associated risks may be a valuable input to budgeting.

2.3 Scope

The scope of the service financial management practice includes:

- defining and communicating an organization’s approach to service financial management

- planning product- and service-related costs and funding, and communicating and controlling budgets

- monitoring the actual costs and funding of products and services

- analysing financial data and providing information for decision-making.

There are some activities and areas of responsibility that are not included in the service financial management practice, although they are still closely related to service financial management. These are listed in Table 2.1, along with references to the practices in which they can be found. It is important to remember that ITIL practices are merely collections of tools to use in the context of value streams; they should be combined as necessary, depending on the situation.

Table 2.1 Activities related to the service financial management practice described in other practice guides

Activity | Practice guide |

Prioritizing funding | Portfolio management |

Defining strategies for the economic aspects of the organization’s products and services | Strategy management |

Tracking valuable IT assets | IT asset management |

Managing financial risks | Risk management |

Negotiating prices with service consumers |

|

Negotiating prices with suppliers |

|

Understanding and recording relationships between the organization’s resources, products, and services |

|

Planning the capacity of products, services, and resources | Capacity and performance management |

Planning and optimization of staffing |

|

2.4 Practice success factors

Definition: Practice success factor |

A complex functional component of a practice that is required for the practice to fulfil its purpose. |

A practice success factor (PSF) is more than a task or activity, as it includes components of all four dimensions of service management. The nature of the activities and resources of PSFs within a practice may differ, but together they ensure that the practice is effective.

The service financial management practice includes the following PSFs:

- ensuring that the organization's service financial management supports its overall strategy and stakeholder requirements

- ensuring that reliable financial information is available as needed to support decision-making.

2.4.1 Ensuring that the organization's service financial management supports its overall strategy and stakeholder requirements

The service financial management practice aims to improve the quality of decisions made in the organization by providing reliable and accurate financial information about the organization’s products and services. This is achieved by following an agreed approach, which should guide all practice activities. There are many options to choose from when defining the approach, from the identification of costs and cost objects to the level of detail needed for budgeting and pricing.

It is important that this practice itself is a form of overhead that increases the costs of the organization’s products and services. Therefore, it is important to balance the benefits created by the practice and its cost; the benefits should exceed the costs.

To achieve this, it is recommended to start planning the service financial management approach by identifying the key stakeholders that will be receiving and using the information. This step and the other steps outlined in Table 2.2 should be guided by the ITIL guiding principles.

Table 2.2 Defining a service financial management approach with the ITIL guiding principles

ITIL guiding principles | Application to the service financial management practice |

| Start where you are | Start by identifying stakeholders and their needs. Do not spend resources n features that do not bring any benefits. |

Focus on value | Analyse currently available information, tools, and procedures. Consider optimising and integrating them before investing resources in a new solution. |

Progress iteratively with feedback | Expand the scope and details of the practice iteratively, with regular and careful consideration of the feedback. The practice has many interconnected parts (for example, budgeting depends on the cost model), so ensure that the first iterations are good enough to continue. |

Collaborate and promote visibility | The quality of the cost data depends on the understanding and readiness to cooperate across the organization. Explain, promote, and engage people to ensure that cost data is accurate, timely, and relevant. Demonstrate the benefits of good service financial management to the stakeholders. |

Think and work holistically | Ensure a holistic understanding of the costs of products and services, considering all types of resources and costs. Do not limit cost and budget models to the data that is easy to get and allocate. At the same time, do not overcomplicate the models. |

Keep it simple and practical | The practice and its models and reports should be as simple and practical as possible. Verify this with the stakeholders; ensure there is no unnecessary data in the reports. Reports should be tailored for the needs of the decision-makers. |

Optimize and automate | Optimize resource-consuming procedures, especially the collection and processing of cost data (particularly related to people’s costs). Where reasonable, automate data collection, processing, and reporting. |

By following these principles, an effective service financial management approach can be created and maintained.

2.4.2 Ensuring that reliable financial information is available as needed to support decision-making

Even where the service financial management practice is a subset of the wider organization’s financial management, it is important to ensure that this practice is not only focused on compliance and control. Its primary focus should be the provision of reliable financial information to the organization’s stakeholders. Management accounts should not be shared outside of organization, and service financial data is often classified as internal or confidential. At the same time, data should be available to the relevant stakeholders when needed in the best form to support decision-making.

To achieve this, the practice should be used in close conjunction with other practices, especially those focused on providing management information. These include:

- knowledge management

- service configuration management

- IT asset management.

In turn, the service financial management practice should inform management decisions in the scope of the other practices, including:

- strategy management

- risk management

- capacity and performance management

- availability management

- service continuity management

- workforce and talent management

- supplier management.

The effective integration of the practices in the organization’s value streams is a key factor for the effectiveness of every practice, stakeholder satisfaction, and the eventual success of the organization.

2.5 Key metrics

The effectiveness and performance of the ITIL practices should be assessed within the context of the value streams to which each practice contributes. As with the performance of any tool, the practice’s performance can only be assessed within the context of its application. However, tools can differ greatly in design and quality, and these differences define a tool’s potential or capability to be effective when used according to its purpose. Further guidance on metrics, key performance indicators (KPIs), and other techniques that can help with this can be found in the measurement and reporting practice guide.

Key metrics for the service financial management practice are mapped to its PSFs. They can be used as KPIs in the context of value streams to assess the contribution of the practice to the effectiveness and efficiency of those value streams. Some examples of key metrics are given in Table 2.3.

Table 2.3 Examples of key metrics for the practice success factors

| Practice success factors | Key metrics |

| Ensuring that the organization's service financial management supports its overall strategy and stakeholder requirements | Stakeholder satisfaction with the financial and economic aspects of the organization's activities Number and impact of cases where a strategic decision could not be executed because of ineffective service financial management Number and impact of audit finding related to service financial management |

| Ensuring that reliable financial information is available as needed to support decision-making | Stakeholder satisfaction with the financial information available Number and impact of cases where the financial information was incorrect or available |

The correct aggregation of metrics into complex indicators will make it easier to use the data for the ongoing management of value streams, and for the periodic assessment and continual improvement of the service financial management practice. There is no single best solution. Metrics will be based on the overall service strategy and priorities of an organization, as well as on the objectives of the value streams to which the practice contributes.

3. Value Streams and processes

3.1 Value stream contribution

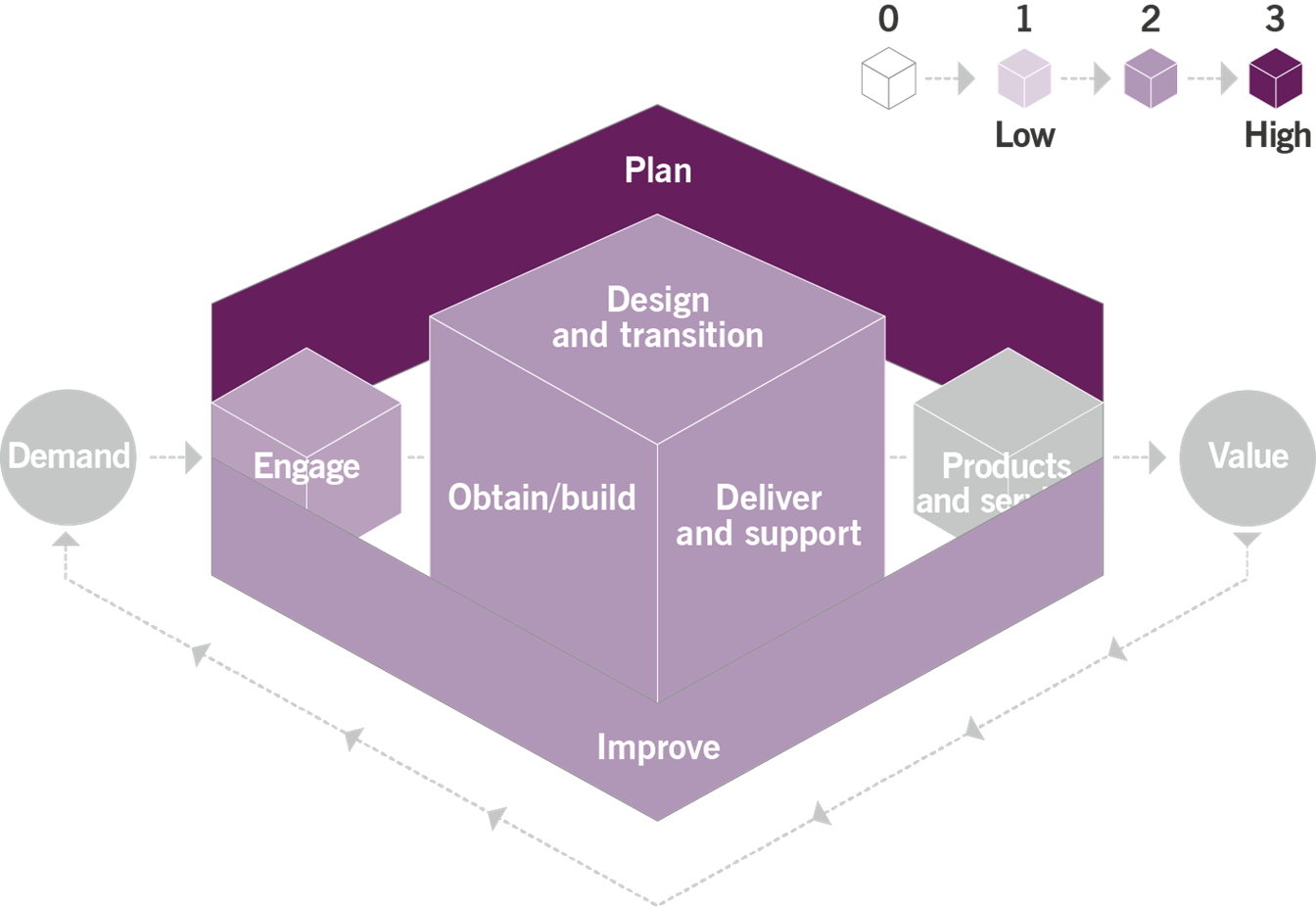

Like any other ITIL management practice, the service financial management practice contributes to multiple value streams. It is important to remember that a value stream is never formed from a single practice. The service financial management practice combines with other practices to provide high-quality services to consumers. The main value chain activity to which the practice contributes is plan. However, all other value chain activities are also impacted by the service financial management practice.

The contribution of the service financial management practice to the service value chain is shown in Figure 3.1.

Figure 3.1 Heat map of the contribution of the service financial management practice to value chain activities

3.2 Processes

Each practice may include one or more processes and activities that may be necessary to fulfil the purpose of that practice.

Definition: Process |

A set of interrelated or interacting activities that transform inputs into outputs. A process takes one or more defined inputs and turns them into outputs. Processes define the sequence of actions and their dependencies. |

Service financial management activities form three processes:

- managing the organization’s approach to service financial management

- financial planning

- management accounting.

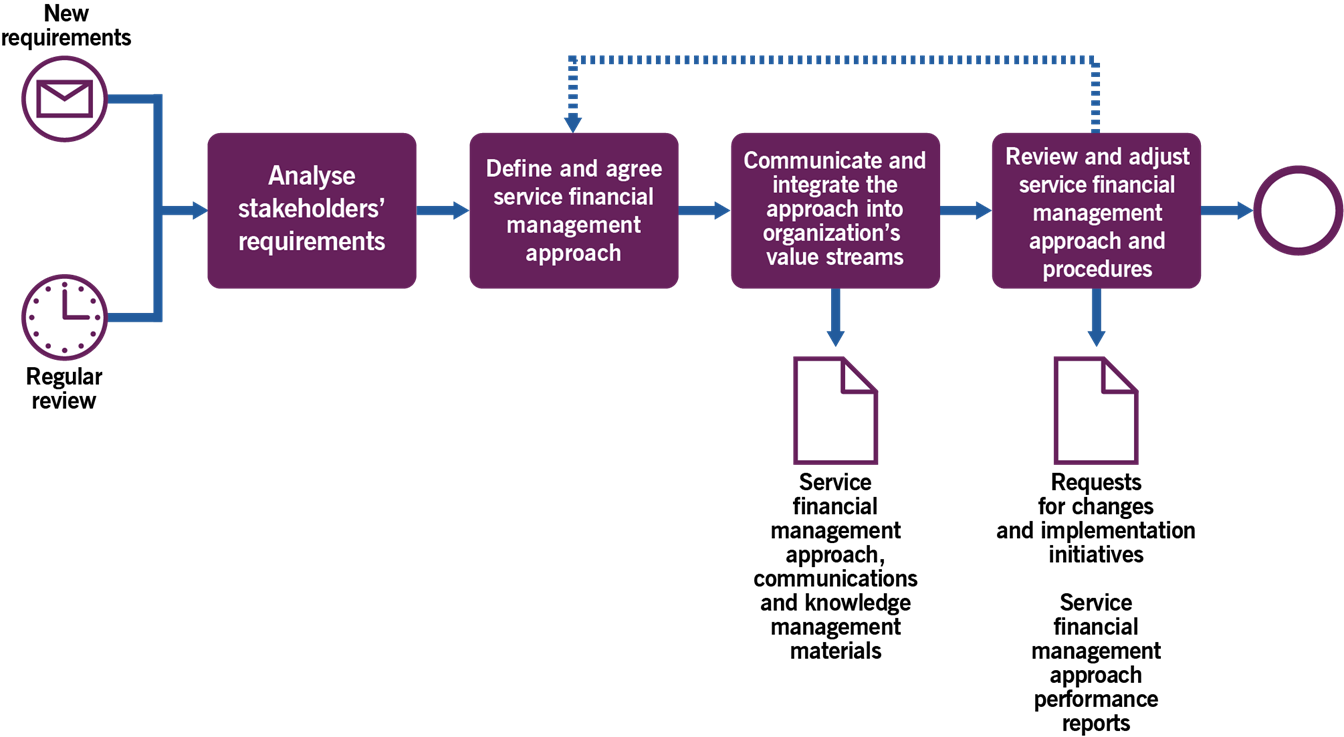

3.2.1 Managing the organization’s approach to service financial management

This process is focused on defining, agreeing, and communicating the organization’s approach to service financial management and embedding the agreed approach in the organization’s value streams and practices.

This process includes the activities listed in Table 3.1 and transforms the inputs into outputs.

Table 3.1 Inputs, activities, and outputs of the managing the organization’s approach to service financial management process

Key inputs | Activities | Key outputs |

|

|

|

Figure 3.2 shows a workflow diagram of the process.

Figure 3.2 Workflow of the managing the organization’s approach to service financial management process

Table 3.2 Activities of the managing the organization’s approach to service financial management process

Activity | An internal IT service provider within a parent organization | An external digital service provider organization |

Analyse stakeholder requirements |

|

|

Define and agree the service financial management approach |

|

|

Communicate and integrate the service financial management approach into the organization's value streams |

|

|

Review and adjust the service financial management approach and procedures |

|

|

3.2.2 Financial planning

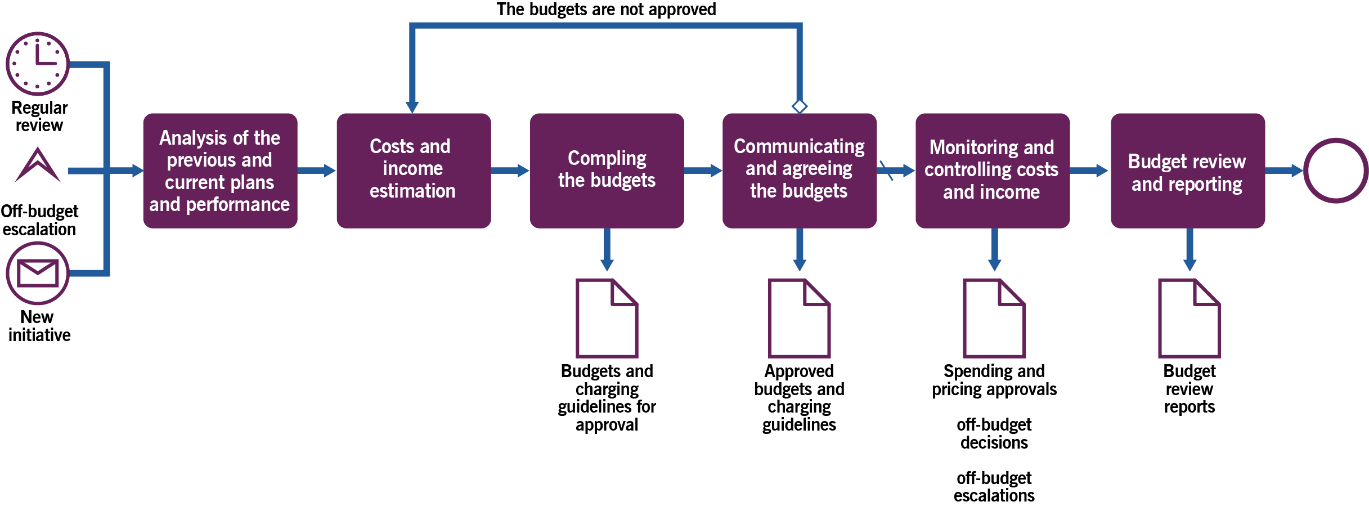

This process is focused on estimating the organization’s costs and income, agreeing and approving budgets, and ensuring that the budgets are properly executed.

This process includes the activities listed in Table 3.3 and transforms the inputs into outputs.

Table 3.3 Inputs, activities, and outputs of the financial planning process

Key inputs | Activities | Key outputs |

|

|

|

Figure 3.3 shows a workflow diagram of the process.

Figure 3.3 Workflow of the financial planning process

Table 3.4 Activities of the financial planning process

Activity | Example |

Analyse the previous and current plans and performance | The service financial team analyses available service financial information, including: current and previous business plans and performance reports

The resulting analysis is used for cost and income estimation. |

Estimate costs and income |

|

Compile the budgets | The team aggregate estimates into budgets following the agreed budget model. |

Communicate and agree the budgets |

|

Monitor and control costs and income |

|

Review and report on the budget | In case of significant deviations from the agreed budgets, the service financial management team (or its dedicated budgeting subset) reviews the affected budgets and initiates a new planning cycle. This is also performed at the end of the budgeted initiatives and periods and on a regular basis: every few weeks to few months, depending on the volatility of the related environment and the performance of the agreed budgets. |

3.2.3 Management accounting

This process is focused on providing management accounting information to the stakeholders. It includes the activities listed in Table 3.5 and transforms the inputs into outputs.

Table 3.5 Inputs, activities, and outputs of the management accounting process

Key inputs | Activities | Key outputs |

|

|

|

Figure 3.4 shows a workflow diagram of the process.

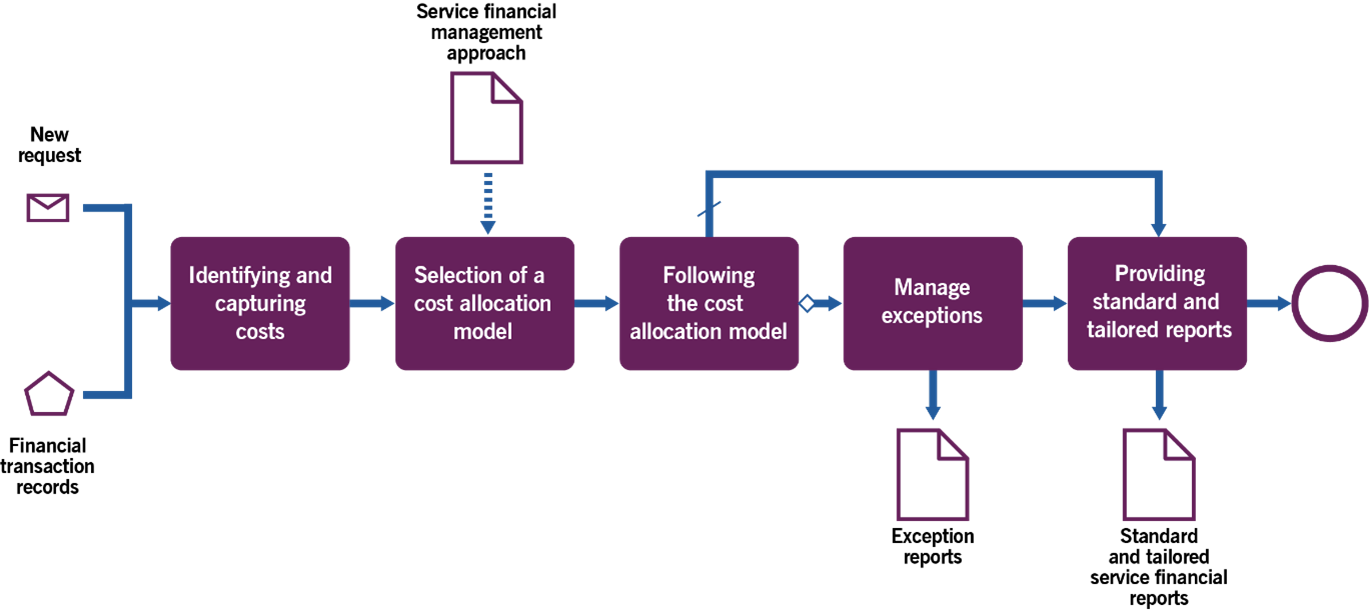

Figure 3.4 Workflow of the management accounting process

Table 3.6 provides examples of the process activities.

Table 3.6 Activities of the management accounting process

Activity | Example |

Identify and capture costs | Following the agreed service financial management approach, the service financial manager(s) identifies and captures data about costs. This task can be largely automated, but manually processing financial records may occasionally be required. |

Select a cost allocation model | The service financial manager(s) selects a cost model from those defined by the service financial management approach to fit the stakeholder requirements. |

Follow the cost allocation model | In line with the selected cost model, the service financial manager(s) performs cost categorization and allocation to produce the information required for the decision-making. |

Manage exceptions | Where necessary, the service financial manager(s) may deviate (within agreed tolerances) from the approved model in order to better meet the stakeholders’ requirements for information. Every exception is reported and serves as input to the continual improvement of the service financial management approach. |

Provide standard and tailored reports |

|

4. Organizations and people

4.1 Roles, competencies, and responsibilities

The practice guides do not describe the practice management roles such as practice owner, practice lead, or practice coach. They focus instead on the specialist roles that are specific to each practice. The structure and naming of each role may differ from organization to organization, so any roles defined in ITIL should not be treated as mandatory or even recommended. Remember, roles are not job titles. One person can take on multiple roles and one role can be assigned to multiple people.

Roles are described in the context of processes and activities. Each role is characterized with a competency profile based on the model shown in Table 4.1.

Table 4.1 Competency codes and profiles

Competency code | Competency profile (activities and skills) |

L | Leader Decision-making, delegating, overseeing other activities, providing incentives and motivation, and evaluating outcomes |

А | Administrator Assigning and prioritizing tasks, record-keeping, ongoing reporting, and initiating basic improvement |

C | Coordinator/communicator Coordinating multiple parties, maintaining communication between stakeholders, and running awareness campaigns |

М | Methods and techniques expert Designing and implementing work techniques, documenting procedures, consulting on processes, work analysis, and continual improvement |

Т | Technical expert Providing technical (subject matter) expertise and expertise-based assignments |

Examples of other roles which can be involved in service financial management activities are listed in Table 4.2, together with the associated competency profiles and specific skills.

Table 4.2 Examples of roles with responsibility for service financial management practice activities

Activity | Responsible roles | Competency profile | Specific skills |

Managing the organization’s approach to service financial management | |||

Analyse stakeholder requirements |

| CT | Excellent knowledge of the organization and stakeholder needs |

Define and agree the service financial management approach |

| MTCA | Good knowledge of financial management theory and practice Excellent understanding of the organization’s architectures, products, and services Good understanding of the stakeholder needs |

Communicate and integrate the service financial management approach into the organization's value streams |

| CLT | Communication and leadership skills |

Review and adjust the service financial management approach and procedures |

| MTCA | Analytical skills Good knowledge of financial management theory and practice Excellent understanding of the organization’s architectures, products, and services Good understanding of the stakeholder needs |

Financial planning | |||

Analyse the previous and current plans and performance |

| TC | Analytical skills Good knowledge of the financial management approach Excellent understanding of the organization’s architectures, products, and services |

Estimate costs and income |

| TCMA | Analytical skills Good knowledge of the financial management approach Excellent understanding of the organization’s architectures, products, and services |

Compile the budgets |

| TA | Good knowledge of the financial management approach |

Communicating and agreeing the budgets |

| CTA | Good knowledge of the budgets Communication skills |

Monitor and control costs and income |

| AT | Good knowledge of the budgets Good understanding of the financial data |

Review and report on the budget |

| TCA | Analytical skills Good knowledge of the financial management approach Good knowledge of the budgets Excellent understanding of the organization’s architectures, products, and services |

Management accounting | |||

Identify and capture costs |

| T | Good understanding of the financial data |

Select a cost allocation model |

| TA | Good knowledge of the financial management approach |

Follow the cost allocation model |

| AT | Good knowledge of the cost model |

Manage exceptions |

| Good knowledge of the financial management approach Good understanding of the financial data | |

Provide standard and tailored reports |

| ACT | Good knowledge of the cost model Good knowledge of the financial management approach |

4.1.1 Service financial manager

The role of the service financial manager is usually performed by team managers, programme and project managers, product owners, or service owners, depending on the service financial management approach adopted by the organization. This role requires the following competencies:

- analytical skills

- knowledge of financial management theory and practice

- good understanding of the organization’s architectures, products, and services

- good understanding of stakeholder needs

- communication skills

- good understanding of financial data.

4.2 Organizational structures and teams

As described in section 2.1, organizational solutions for the service financial management practice depend on the role of IT and IT management in the organization. Depending on this, the solutions may involve:

- including financial professionals (finance business partners) in digital product teams, focusing on the service financial management practice

- including digital and IT business partner(s) within the finance team, focusing on digital products and services

- including a dedicated finance team within the IT department, focusing on the service financial management practice and collaborating with the finance team in the wider organization

- providing special training and education in the service financial management practice for product and service managers and IT leaders.

5. Information and technology

5.1 Information exchange

The effectiveness of the service financial management practice is based on the quality of the information used. This includes, but is not limited to, information about:

- the organization’s strategy

- stakeholders’ needs and requirements

- the organization’s architectures

- the organization’s portfolios

- partners and suppliers

- key service offerings and service consumers

- the automation of financial transactions in the organization

- the organization’s ongoing performance.

This information may take various forms. The key inputs and outputs of the practice are listed in section 3.

5.2 Automation and tooling

The service financial management practice is not usually perceived as highly automated. However, it can significantly benefit from the opportunities offered by advanced analytics, big data, modelling, and forecasting. Collaboration and communication tools are also useful for every activity of the practice. Table 5.1 lists the specific means of automation that are relevant to each practice activity.

Table 5.1. Automation solutions for service financial management activities

Activity | Means of automation | Key functionality | Impact on the effectiveness of the practice |

Managing the organization’s approach to service financial management | |||

Analyse stakeholder requirements | Collaboration tools | Gathering and analysing requirements | Medium |

Define and agree the service financial management approach |

|

| High |

Communicate and integrate the service financial management approach into the organization's value streams |

|

| High |

Review and adjust the service financial management approach and procedures |

|

| High |

Financial planning | |||

Analyse the previous and current plans and performance |

|

| High |

Estimate costs and income |

| Data modelling, forecasting, planning, and visualization | High |

Compile the budgets |

| Compiling, managing, and presenting budgets | High |

Communicate and agree the budgets |

| Sharing budgets with limited groups of people for collaboration and approval | Medium |

Monitor and control costs and income |

| Mapping financial records associated with resources, products, services, and associated budgets | High |

Review and report on the budget |

| Data modelling, forecasting, planning, and visualization | High |

Management accounting | |||

Identify and capture costs |

| Mapping financial records associated with resources, products, services, and associated cost models | High |

Select a cost allocation model |

| Managing cost models | High |

Follow the cost allocation model |

| Mapping financial records associated with resources, products, services, and associated cost models | High |

Manage exceptions |

| Mapping financial records associated with resources, products, services, and associated cost models | High |

Provide standard and tailored reports |

| Creating and presenting dashboards and reports | High |

6. Partners and suppliers

Very few products and services are delivered using only an organization’s own resources. Most, if not all, depend on other products and services, often provided by third parties outside the organization (see section 2.4 of ITIL Foundation: ITIL 4 Edition for a model of a service relationship). This implies that financial data about third-party resources and services is important for a correct and full understanding of the costs of an organization’s resources, products, and services. Furthermore, its importance is growing as more and more organization’s resources are replaced by third-party services (for example, cloud or outstaffing).

It is important to note that the service financial management information produced by this practice is largely specific to the organization; it is sensitive and usually confidential. This limits the use of third-party services to support the practices with consulting and automation, with strict rules regarding data sharing and distribution.

7. Important reminder

Most of the content of the practice guides should be taken as a suggestion of areas that an organization might consider when establishing and nurturing their own practices. The practice guides are catalogues of things that organizations might think about, not a list of answers. When using the content of the ITIL practice guides, organizations should always follow the ITIL guiding principles:

- focus on value

- start where you are

- progress iteratively with feedback

- collaborate and promote visibility

- think and work holistically

- keep it simple and practical

- optimize and automate.

More information on the guiding principles and their application can be found in section 4.3 of ITIL Foundation: ITIL 4 Edition.

8. Acknowledgements

AXELOS Ltd is grateful to everyone who has contributed to the development of this guidance. These practice guides incorporate an unprecedented level of enthusiasm and feedback from across the ITIL community. In particular, AXELOS would like to thank the following people.

8.1 Author

Roman Jouravlev.

8.2 Contributors

David Cannon, Pavel Demin, Dmitry Isaychenko.

8.3 Reviewers

David Cannon, David Crouch, Irina Matantseva, Dmitriy Isaychenko, Anton Lykov, Alex Stupnikov.